What can it all mean when mega-cap stocks and US Treasuries start behaving as if they were penny stocks?

Tavis McCourt, Institutional Equity Strategist at Raymond James, has an idea about that. “We would argue it shows a complete lack of conviction by investors in certain business models/earnings power, and the state of the economy overall,” McCourt wrote.

McCourt is talking of the spell of extreme volatility the markets are currently going through, noting that investors can’t make up their minds whether we will see a multi-year economic recovery or whether we will soon enter a “Fed induced” recession.

Investor psychology is changing on a weekly – or even daily – basis. As such holding on to your investment convictions has never been harder – or more painful. That said, McCourt adds that sticking to your guns is essential in “driving outperformance.”

Against this backdrop, the analysts at Raymond James have been seeking out stocks that are aimed to push ahead in the current environment. They have pinpointed two which they see generating returns of at least 60% this year.

We ran them through the TipRanks database to see what the rest of the Street thinks; it appears the analyst consensus rates both as Strong Buys and sees plenty of upside too. Let’s take a closer look.

ADS-TEC Energy †ADSE†

We’ll start in the energy sector, where ADS-TEC is a leader in decentralized battery-buffered power systems. The company designs, manufactures, and markets a range of battery management systems, power inverters, thermal management units, and control systems. The ADS-TEC platforms always include a ‘smart’ battery storage system, allowing for flexible absorption and release of energy, making the units highly adaptable. The company’s products have found uses in industry, commerce, mobility, and infrastructure applications.

A key element in the ADS-TEC product portfolio is the fast charging technology, allowing for rapid charging of mobility battery solutions, even when the power grid performance is low. The company’s technology permits ultra-fast charging of storage batteries up to 320 kilowatts. ADS-TEC has delivered more than 400 such charging systems, which are particularly suited to the EV industry.

This company has been a public entity since the end of December, when it completed a SPAC merger with European Sustainable Growth Acquisition Corporation. The merger, which made $152 million in new capital available to ADS-TEC’s development program, was approved on December 21 and the ADSE ticker made its NASDAQ debut on December 23.

In his initiation of coverage report for Raymond James, 5-star analyst Pavel Molchanov lays out a bullish case for ADS-TEC, writing: “Charging infrastructure across the board is an underappreciated factor for the light-duty electric vehicle adoption curve, but charging technology is not a cookie-cutter story. At the leading edge is ultra-fast charging, and ADS-TEC stands out as the only public pure-play on this small but rapidly growing slice of the pie. We favor the company’s above-average exposure to Europe, which has the world’s highest EV market share. As with all clean tech hardware, some commoditization is inevitable. With shares trading below 10x our (relatively conservative) 2025 EBITDA estimate, we think the entry point is compelling…”

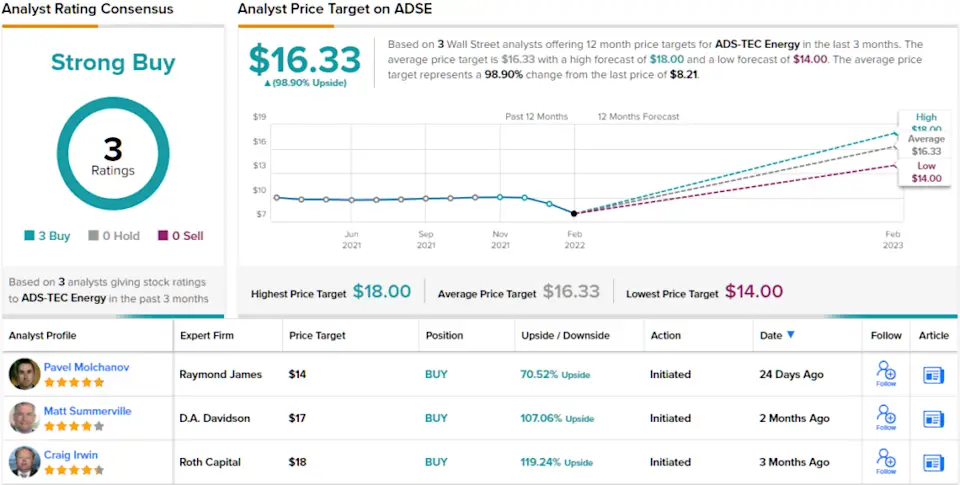

Based on all of the above factors, Molchanov rates ADSE shares a Strong Buy and his $14 price target implies a one-year upside potential of ~71%. (To watch Molchanov’s track record, click here†

In its short time on the public markets, this fast-charging tech firm has picked up 3 positive analyst reviews, for a unanimous Strong Buy consensus rating. The shares are priced at $8.21 and their $16.33 average price target is even more bullish than the Raymond James view, indicating room for ~99% upside in the coming year. †See ADSE stock analysis on TipRanks†

ProQR †PRQR†

The second stock we’re looking at is a biotech research firm. ProQR is working on new medications to treat a related group of genetic sight disorders, the inherited retinal diseases. These eye diseases have no effective treatments, are progressive in nature, and typically lead to blindness.

The company’s development pipeline features RNA therapies, novel treatments for a range of genetically based disorders. The pipeline has four clinical-stage programs, as well as several preclinical research tracks. The leading drug candidate, sepofarsen (QR-110), was the subject of the Phase 2/3 ILLUMINATE clinical trial, evaluating the drug as a treatment for Leber congenital amaurosis 10 (LCA10).

In a major update early last month, ProQR announced that the last patient in the ILLUMINATE trial has completed the final 12-month visit, an important milestone toward developing full top-line results. The company is expected to release those results by the end of the current quarter, 1Q22. The study followed 36 randomized patients, starting in January of 2021.

Also of interest for investors, ProQR announced in December the beginning of two additional Phase 2/3 trials, evaluating ultevursen (QR-421a) as a treatment for mediated retinitis pigmentosa and Usher syndrome. The first patients have been dosed in these two trials, dubbed SIRIUS and CELESTE, which are expected to continue for the next 24 months. The SIRIUS trial will enroll up to 81 patients, while the CELESTE trial is designed for 120 patients.

Analyst Steven Seedhouse opened coverage of this stock for Raymond James with a bullish stance, pointing out the strength of the company’s development tracks.

“LCA10 is a ~$390M WW market opportunity for sepofarsen and opens door for rest of ProQR’s IRD pipeline, including QR-421a, which is in pivotal studies for Usher syndrome and retinitis pigmentosa. The data for QR-421a aren’t as impressive as sepofarsen but it could still work, and Phase 1 extension data expected in late 2022 could add confidence… The three pillars of our investment thesis are: 1) positive view on near-term pivotal trial catalyst (CEP290 targeting oligo in LCA10), data 1Q22; 2) additional clinical stage programs could become derisked near term; and 3) leadership in emerging area where we want immediate exposure (RNA editing),” Seedhouse opined.

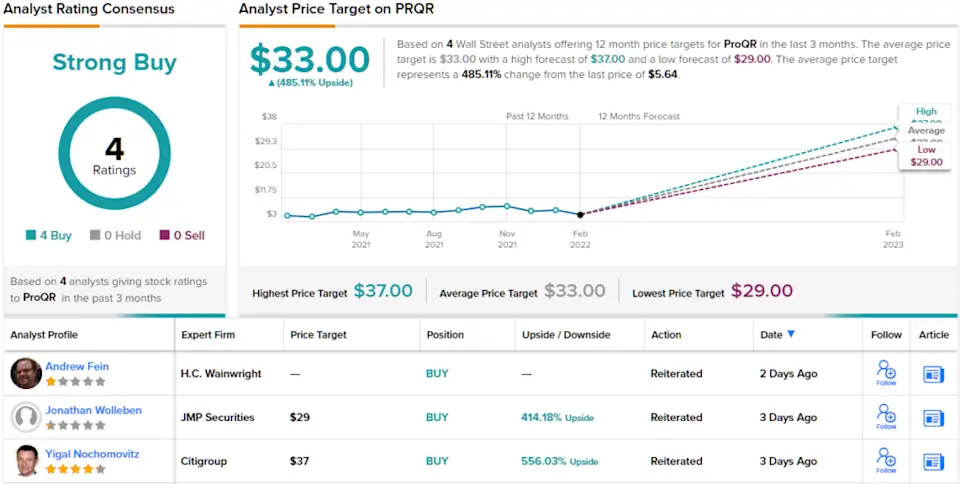

In light of these comments, Seedhouse rates PRQR stock as a Strong Buy, and sets a $19 price target that suggest the shares have room to run up a robust ~237% this year. (To watch Seedhouse’s track record, click here†

All in all, the Strong Buy consensus view on ProQR is unanimous, as all 4 analyst reviews take a positive stance. The stock is priced at $5.64 and has a $33 average price target; this implies one-year upside potential of a huge 485%. †See PRQR stock forecast on TipRanks†

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buya newly launched tool that units all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.